Unlock Growth with finance restaurant equipment: Smart Funding Options

Figuring out how to pay for your kitchen equipment is a huge step for any Los Angeles food business. It doesn't matter if you're launching a Korean BBQ spot in K-Town, a trendy Mexican food truck destined for Silver Lake, or just upgrading a beloved Chinese restaurant in the San Gabriel Valley. The financing path you choose is about more than just money—it’s about setting your business up for growth.

Your choice here affects everything from your monthly cash flow to how quickly you can expand down the road. Let’s break down the landscape so you can find the right strategy without getting bogged down in confusing jargon.

Your Guide to Financing Kitchen Equipment in Los Angeles

Before you start filling out applications or comparing interest rates, you need to get a handle on the basic differences between your options. Think of it like picking the right tool for the job. You wouldn't use a wok to bake a pizza, right? The same logic applies here. The best way to fund a brand-new walk-in freezer is probably different from how you'd pay for smaller warewashing items.

Here are the main paths you'll run into:

- Traditional Bank Loans: Best for established restaurants with solid credit. You get full ownership and usually lower long-term costs.

- SBA-Backed Loans: A great fit for startups or businesses that might not qualify for a traditional loan. The terms are often better, but the application process can be a bit more involved.

- Equipment Leasing: A popular choice for new spots or Los Angeles food trucks. This option keeps more cash in your pocket with lower upfront costs and predictable monthly payments.

- Business Line of Credit: This gives you flexible, revolving credit for ongoing or surprise equipment needs, like when a commercial refrigerator dies mid-service.

Choosing the right financing means you can get that essential Atosa commercial refrigerator or freezer without draining the cash you need for daily operations. In a fast-paced market like L.A., that's everything.

To give you a clearer picture, here’s a quick comparison of the primary financing methods available to Los Angeles restaurant owners. This should help you decide which path makes the most sense to explore first for your business.

Financing Options at a Glance

| Financing Type | Best For | Typical Ownership | Credit Impact |

|---|---|---|---|

| Traditional Loan | Established businesses with strong credit history. | Full ownership from day one. | Builds business credit; significant initial inquiry. |

| SBA Loan | Startups or those needing more favorable terms. | Full ownership after the loan is paid off. | Builds business credit; lengthy approval process. |

| Equipment Lease | New ventures, businesses conserving cash, or those needing the latest tech. | Option to own at the end of the lease term. | Lower initial impact; consistent payment history builds credit. |

| Line of Credit | Unexpected repairs, short-term needs, or ongoing smaller purchases. | Not applicable; it's a credit line, not an asset purchase. | Can impact credit utilization; good for flexibility. |

Each of these options serves a different purpose. A loan might be perfect for a long-term investment in a cornerstone piece of equipment, while a lease gives you the flexibility to upgrade as technology changes.

The Growing Need for Modern Equipment

Making the decision to finance is more relevant than ever. The global market for restaurant equipment is booming, projected to jump from $3.88 billion in 2024 to $5.58 billion by 2029.

What's driving this? For one, rapid urbanization in cities like Los Angeles and stricter food safety regulations are pushing restaurants to upgrade. Operators need more efficient gear, like compact under-counter refrigerators, to keep up. For L.A. owners, this trend just underscores how important it is to invest in modern, reliable equipment to stay competitive. You can read the full research about the restaurant equipment market to get a deeper dive.

Choosing the Right Financing Path for Your Restaurant

Figuring out how to pay for restaurant equipment isn't just a numbers game. It's about finding the right fit for your business, your goals, and your reality on the ground. A full-service Japanese spot in Little Tokyo has completely different needs than a brand-new Korean food truck, and their financing should reflect that.

Let’s walk through a few real-world Los Angeles scenarios to see which path makes the most sense for your vision. Each option has its ups and downs, and knowing the difference is the first step toward making a smart financial move.

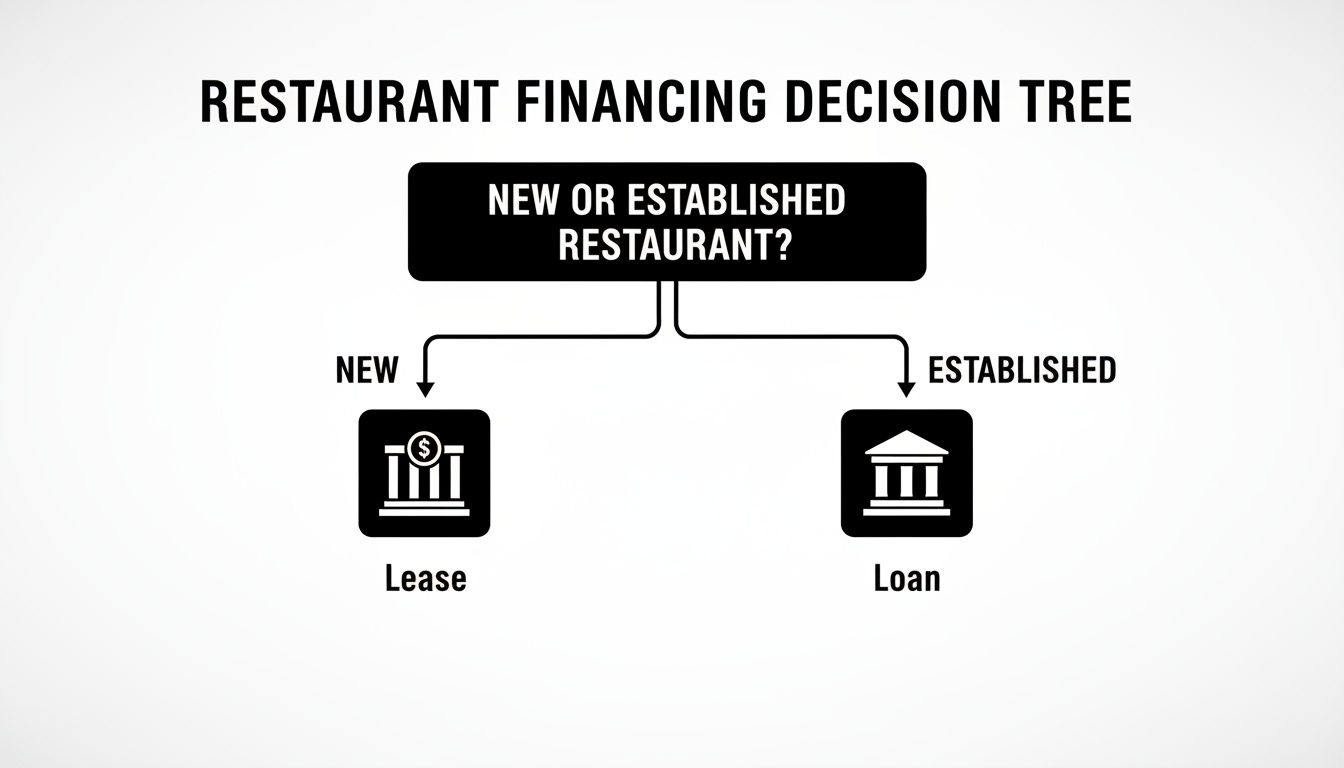

This decision tree gives you a quick visual on the main financing routes for new versus established restaurants.

As you can see, brand-new businesses often lean toward leasing to protect their cash flow. On the other hand, established restaurants with solid financials might find that a traditional loan is a better play for building equity.

The Traditional Bank Loan Scenario

Picture this: an established Japanese restaurant in Little Tokyo is ready for a complete kitchen overhaul. They've been around for over a decade, business is booming, and they need new ranges, commercial refrigerators, and a high-capacity ice maker to keep up. With a history of profitability and great credit, a traditional bank loan is a fantastic option.

- Pros: The biggest win here is immediate ownership. The equipment becomes an asset on their balance sheet right away. Plus, over the long haul, they'll likely pay less thanks to competitive interest rates, which usually fall between 6% to 9%.

- Cons: The catch is the approval process. It's notoriously slow and paperwork-heavy, demanding years of financial statements, tax returns, and a detailed business plan. Those strict credit requirements can be a dealbreaker for newer businesses.

This path is really built for well-capitalized restaurants with a proven track record that are looking to make a serious, long-term investment in their kitchen.

The SBA Loan for a Startup Food Truck

Now, let's switch gears to a new Mexican food truck entrepreneur. They've got an amazing concept but not much of an operating history. They need to outfit the entire truck—griddles, fryers, prep tables, the whole nine yards. A traditional bank loan is probably a non-starter, but an SBA-backed loan could be the perfect solution.

The Small Business Administration steps in to guarantee a part of the loan, which makes lenders feel a lot more comfortable working with a startup. This often translates to better terms, like a lower down payment and a longer repayment period (up to 10 years for equipment), which keeps those monthly payments from becoming a burden.

The trade-off? The application process is even more of a beast than a standard bank loan, so you have to be ready to put in the work.

Key Takeaway: SBA loans are the lifeline for many new and growing businesses that wouldn't get funding otherwise. They fill a crucial gap for passionate entrepreneurs ready to bring their dreams to the streets of Los Angeles.

Equipment Leasing for a Quick-Service Cafe

Think about a new Thai quick-service cafe opening up near UCLA. Their priority is getting the doors open fast while keeping as much cash on hand as possible for things like marketing and payroll. For them, equipment leasing is a brilliant strategic move.

Instead of dropping a huge chunk of change on Atosa prep tables and commercial freezers, they make predictable monthly payments. This keeps their cash flow healthy during those critical first few months when every dollar counts.

- Low Upfront Cost: This frees up capital for all the other things a new business needs.

- Flexibility: When the lease is up, they have options. They can buy the equipment, upgrade to the latest models, or simply return it.

- Easier Approval: Getting approved is often faster and less of a headache than a loan, since the equipment itself is the collateral.

Leasing is a powerful tool for startups and any business that needs to stay nimble. It helps you avoid getting stuck with equipment that could be outdated in a few years. While the total cost might be higher in the long run compared to a loan, the immediate cash-flow benefits are hard to beat. To stretch the budget even further, many owners also check out used restaurant equipment in Los Angeles.

A Line of Credit for a Catering Company

Finally, let's consider a busy Chinese food catering company over in the San Gabriel Valley. Their equipment needs can change from one week to the next depending on their event schedule. This is where a business line of credit offers incredible flexibility.

It basically works like a credit card for the business. They can draw funds whenever they need to buy smaller items—like a new deep fryer before a big wedding—and only pay interest on what they’ve used. It's the perfect solution for handling unexpected repairs or jumping on a good deal for equipment without having to go through a whole new loan application every time.

Cooking equipment is the heart of the kitchen, making up over two-thirds of the foodservice market's revenue in 2023. Busy full-service restaurants and hotels are always in need of reliable ranges, griddles, and ovens. If you want to dive deeper into the different funding options out there, it's worth checking out a comprehensive guide to restaurant equipment financing. In a competitive market like Los Angeles, you always have to be ready for both planned upgrades and last-minute replacements.

Preparing Your Loan Application Package

Walking into a lender's office unprepared is a lot like showing up for dinner service without your key ingredients prepped. It just doesn't work. To successfully finance your restaurant equipment, you need to hand over a complete and compelling story of your business. A well-organized application package isn't just about checking off boxes; it’s about building confidence and showing the lender you're a serious, organized operator who knows their numbers.

Think of your application as the business plan for this specific, crucial investment. It needs to clearly explain what you need, why you need it, and exactly how it’s going to make you money. Honestly, this level of preparation can be the difference between a quick "yes" and a frustrating "no."

Crafting a Compelling Business Plan

Your business plan is the narrative of your restaurant's journey. This is where you connect the dots for the lender, showing them precisely how a piece of new equipment will fuel your growth. For a new Korean food truck, this means explaining how a high-capacity charbroiler will let you serve more customers during that chaotic lunch rush.

Get specific about the impact. For example, detail how a new Atosa commercial freezer will allow you to buy ingredients in bulk, cutting your food costs by 5-7%. Or, explain how a new ice maker will support an expanded craft cocktail program you project will boost sales by 10%. These concrete numbers turn a simple request into a smart investment strategy they can get behind.

Gathering Your Financial Documents

Lenders need a crystal-clear view of your financial health. Vague estimates and ballpark figures won't cut it here. You’ll need to put together a detailed file that paints a complete picture of your restaurant's past performance and current stability.

Your financial document checklist should absolutely include:

- Profit & Loss (P&L) Statements: Have at least two to three years of P&L statements ready to go. These show your revenue, costs, and profitability over time.

- Balance Sheets: These give a snapshot of your assets and liabilities, giving the lender a good look at your overall financial position.

- Cash Flow Statements: This one is crucial. It shows how cash moves in and out of your business, proving you can handle a new monthly payment without breaking a sweat.

- Business and Personal Tax Returns: Most lenders will ask for at least two years of returns for both the business and its principal owners.

I’ve seen it happen time and again: a common mistake is submitting incomplete or disorganized financials. Lenders review hundreds of applications; making their job easier with a clean, comprehensive package significantly improves your chances.

The Importance of a Specific Equipment Quote

Don't just walk in asking for a generic "refrigerator loan." Lenders need to know exactly what they are financing. This is why providing a detailed quote from a supplier like Los Angeles Restaurant Equipment is non-negotiable.

For instance, submitting a formal quote for an Atosa two-door commercial freezer and a matching ice maker shows you've done your homework. It gives the lender a precise dollar amount to work with and proves the equipment's value lines up with your loan request. This kind of specificity removes any doubt and helps the lender see the equipment as a tangible asset that secures their investment. If you need a hand creating a wish list, check out our guide on building a commercial kitchen equipment checklist.

Essential Legal and Business Paperwork

Finally, you'll need to round out your package with all the necessary legal documents. This is the stuff that verifies your business's legitimacy and proves you're operating by the book. It’s the foundation that your entire application rests on.

Make sure you have copies of:

- Business Licenses and Permits: This includes your City of Los Angeles business license and any health department permits.

- Articles of Incorporation/Organization: This applies if your business is an LLC or a corporation.

- Commercial Lease Agreement: Your lease shows the lender you have a stable location for your operations, which is a big deal.

- Business Bank Statements: Provide three to six months of recent statements to show consistent, healthy cash flow.

By getting all these documents together beforehand, you present yourself as a proactive and reliable partner, making the decision to finance your restaurant equipment an easy one for any lender.

How to Improve Your Approval Odds

Getting a "yes" from a lender is about so much more than just filling out paperwork. You need to strategically position your Los Angeles restaurant as a solid, profitable investment they can get behind. Lenders are always on the lookout for signs of stability and smart financial management.

Think of it this way: a lender is betting on your success. It’s your job to give them every reason to feel confident placing that bet. That means getting your financial house in order before you even start shopping for that essential commercial refrigerator or freezer.

Strengthen Your Credit Score

Your personal and business credit scores are the very first things a lender is going to pull. A strong score tells them you have a history of managing debt responsibly. If your score isn't quite there yet—you’re ideally aiming for 680 or higher for traditional loans—it’s time to get to work.

Start by paying all your bills on time, every single time. Late payments can seriously drag your score down. Next, focus on paying down existing debt, especially those high-interest credit card balances, which will lower your credit utilization ratio. And don't forget to check your credit report for errors; correcting them is a quick win that can give you a nice boost.

Show Them the Money with a Larger Down Payment

Nothing speaks louder to a lender than a sizable down payment. When you put more of your own money down upfront, you reduce the amount you need to finance, which immediately lowers the lender's risk. It proves you have skin in the game and shows real financial discipline.

For a Los Angeles food truck owner, putting down 20-25% on a new set of Atosa cooking equipment instead of the bare minimum 10% can completely change a lender’s perspective. It tells them you have the cash reserves to handle a slow month and makes you a much more attractive borrower. This one move can often unlock better interest rates and more favorable terms.

A larger down payment is a powerful signal to lenders. It says, "I am invested in this, I have managed my cash well, and I am not over-leveraging my business." This confidence can be the deciding factor in your approval.

Demonstrate Consistent Cash Flow

Beyond your credit score, lenders need to see proof of strong, consistent cash flow. They need to be sure you can comfortably take on a new monthly payment without putting a strain on your operations. This is where meticulous bookkeeping becomes your best friend.

To really improve your odds, lenders want clear evidence of sound financial management. That means knowing how to categorize business expenses for smarter budgeting. Organized financial statements that clearly show steady revenue and healthy profit margins are non-negotiable.

Imagine you're running a busy Mexican restaurant in East L.A. If your bank statements show erratic deposits and frequent low balances, a lender is going to get nervous. Consistent, predictable income tells a story of a well-run business that can handle new debt responsibly.

Consider a Lease-to-Own Option

If your credit is less than perfect or you're a newer business without years of financial history, don't get discouraged. A lease-to-own program can be a much more accessible way to get the equipment you need right now. For many Thai and Chinese restaurants in L.A., this is the go-to route for acquiring new gear.

Here’s why it works so well:

- Collateral is Built-In: The equipment itself—whether it's an Atosa commercial freezer or a pizza prep table—serves as the collateral. This dramatically reduces the risk for the leasing company.

- Approval is Easier: Because the risk is lower, the approval criteria are often much more flexible than what you'd find at a traditional bank.

- Credit Building Opportunity: Making your lease payments on time, every time, is a fantastic way to build up your business credit profile. This sets you up for even easier financing approvals down the road.

This path allows you to get the high-quality restaurant equipment you need to grow your business, all while strengthening your financial standing for the long term.

The Strategic Advantage of Leasing Equipment

For any L.A. food entrepreneur, especially if you're getting a food truck or ghost kitchen off the ground, cash is king. Every single dollar has to pull its weight. Tying up all your precious capital in equipment from day one often isn't the smartest move. This is where leasing, and specifically lease-to-own financing, becomes a seriously powerful tool for getting your kitchen kitted out.

Leasing lets you get your hands on the high-performance gear you need—from that essential Atosa commercial refrigerator to a workhorse convection oven—without a massive upfront cash drain. Instead of one huge payment, you have predictable monthly payments. This lines up your equipment costs with the money coming in, which is an absolute lifesaver for a new Thai pop-up or a growing Chinese restaurant trying to keep a handle on cash flow.

Hold Onto Your Capital and Fuel Growth

The single biggest win with leasing is holding onto your working capital. The cash you don't spend buying a commercial freezer outright can be poured right back into the things that actually grow your business: marketing your K-town BBQ joint, hiring another line cook, or sourcing better ingredients for your sushi bar.

Think about it. A typical equipment loan might ask for a 10-20% down payment, which can easily run into thousands of dollars. A lease? You’re often just looking at the first and last month's payment to get started. That’s a huge difference that frees you up to invest where it counts, especially in those make-or-break first few years.

To really see the difference, let's look at a common scenario for an L.A. kitchen: getting a new commercial refrigerator.

Loan vs. Lease-to-Own: A Cost Scenario for a Commercial Refrigerator

| Financial Metric | Traditional Loan Example | Lease-to-Own Example |

|---|---|---|

| Equipment Cost | $4,000 | $4,000 |

| Upfront Cash | $800 (20% down payment) | $300 (First & last month's payment) |

| Monthly Payment | $145 (36 months @ 8% APR) | $150 (36 months) |

| Total Cost to Own | $5,220 | $5,500 (incl. $100 buyout) |

| Initial Capital Saved | - | $500 |

As you can see, while the total cost of the lease might be slightly higher over the long run, the immediate benefit is crystal clear: $500 in extra cash stays in your pocket. For a new business, that cash is far more valuable for inventory, marketing, or payroll than it is tied up in a down payment.

Build Up Your Business Credit Profile

For any new business trying to make it in the competitive L.A. food scene, building a solid credit profile is a marathon, not a sprint. A lease-to-own agreement is a fantastic way to get a head start. Every on-time payment you make gets reported to the business credit bureaus, which helps build a positive payment history one month at a time.

This creates a powerful ripple effect. As your business credit score climbs, you start looking a lot more attractive to lenders for other types of financing you'll need down the road, like a business line of credit or a loan to open a second location. It’s a smart way to strengthen your restaurant’s financial legs while getting the gear you need to operate.

For a startup, leasing isn't just a financing method; it's a credit-building strategy. Consistent payments demonstrate financial responsibility, opening doors to better funding opportunities as you scale.

Gain Flexibility and Avoid Outdated Tech

The food industry moves fast, and so does its technology. The super-efficient commercial refrigerator that’s top-of-the-line today could be old news in five years. Leasing gives you an incredible amount of flexibility that owning equipment just can't offer.

When your lease term is up, you've got options:

- Buy the Equipment: If that piece of gear is still a workhorse for your Mexican food truck, you can buy it out, usually for a pre-agreed price.

- Upgrade to Newer Models: Start a new lease with the latest, more energy-efficient models. This keeps your kitchen modern and your utility bills down.

- Return the Equipment: Maybe your menu changed and you don't need that specific item anymore. Just return it without the headache of trying to sell it on the second-hand market.

This flexibility means you’re not stuck with outdated or inefficient tech. You can learn more about how a restaurant equipment lease-to-own program works to see if it’s the right call for your business. It's a savvy way to stay agile in the constantly shifting L.A. dining scene.

Common Questions About Equipment Financing

Diving into equipment financing can feel overwhelming, especially in a market as fast-paced as Los Angeles. Whether you're getting a new Korean food truck on the road or finally upgrading your beloved Thai restaurant, getting straight answers is the first step. Here are a few of the questions we hear all the time from L.A. restaurateurs.

What Credit Score Do I Need?

There’s no single magic number that opens every door. For a traditional bank loan, lenders are usually looking for a personal credit score of 680 or higher. A score like that tells them you have a solid track record of managing your finances well.

But don't get discouraged if your score isn't quite there. Alternative lenders and equipment leasing companies can be much more forgiving. Since the equipment itself—say, a brand-new Atosa commercial freezer—serves as the collateral, their risk is naturally lower. It’s not uncommon for them to approve applications for owners with scores in the low 600s, which is a huge help for new businesses just starting out.

Can I Finance Used Restaurant Equipment?

Absolutely, but you should expect a few extra hoops to jump through. Most traditional banks get a little skittish when it comes to used equipment. It’s tough for them to nail down its true value and how much life it has left, making it feel like a risky bet.

You’ll have better luck with specialized equipment financing companies or certain online lenders who are more comfortable with the pre-owned market. If you decide to go this route, make sure you’re buying from a reputable dealer who can give you a full condition report.

Honestly, a smarter long-term move, especially for a new spot, is leasing new equipment. It comes with a full warranty, saving you from those soul-crushing, unexpected repair bills that can sink a restaurant's budget before it even gets going.

How Long Does The Financing Process Take?

The time it takes to get from application to funded can be wildly different depending on which option you choose. You’ll want to build this timeline into your business plan, particularly if you’re on a tight schedule to open your new Chinese restaurant or Japanese sushi bar.

Here’s a quick look at what you can expect:

- SBA Loans: These have some of the best terms available, but they are by far the slowest. Plan on waiting 60 to 90 days from application to funding.

- Traditional Bank Loans: A little quicker, but still a process. These usually take anywhere from 2 to 6 weeks to get fully approved and funded.

- Online Lenders & Leasing: This is the fastest path, hands down. You can often get an approval in just 24-48 hours and have your equipment funded and on its way in no time. That speed is a lifesaver when your commercial refrigerator suddenly dies.

What If My Restaurant Closes Before The Financing Is Paid Off?

It's a tough thought, but a necessary one in the high-stakes L.A. food scene. What happens next really comes down to the type of financing you have.

If you took out a traditional loan, you almost certainly signed a personal guarantee. This is a big deal. It means that if the business fails, you are still personally responsible for paying back the rest of the debt. The lender can pursue business assets and, in some cases, your personal assets like your house or car.

An equipment lease, on the other hand, usually builds in a layer of protection. If the business has to close, the leasing company simply comes and repossesses the equipment to recover their investment. While it will still impact your business credit, it generally keeps your personal assets out of the picture. For new ventures like a Mexican food truck, that peace of mind is priceless.

Ready to get the essential equipment your L.A. restaurant needs without draining your capital? Los Angeles Restaurant Equipment offers flexible lease-to-own financing on top-tier brands like Atosa, helping you conserve cash, build business credit, and get your kitchen running fast. Explore our full catalog and financing options today at https://losangelesrestaurantequipment.com.